How machine learning is transforming trading

Judging by the level of activity in the banking industry, machine learning is on its way to being the next big innovation to hit the trading desk. Leading banks are diving into the field, building up their expertise in machine learning, running trials in their innovation labs, and exploring ways to use this form of artificial intelligence to transform the trading process.

According to consulting firms that are tracking this trend, machine learning is already being deployed to help identify trading signals, optimize market-making, anticipate trade breaks, and improve the interaction between banks and their clients.

The potential impact could be as big as the algorithmic trading revolution that swept through the industry a decade ago. Just as the use of algorithms led to ultra-fast quoting engines and more efficient execution of trades, machine learning could lead to another wave of automation as intelligent computers take over more elements of the trading process.

It is hard to be certain about how much progress is being made, however. The deployment of machine learning in capital markets is still at an early stage and the scale of the deployment appears to be limited to specific use cases, at least for now. In fact, some experts say that the trading environment poses an especially difficult challenge for machine learning. It’s one thing for a machine to learn how to win a game of chess. It’s quite another to beat the market.

"In the financial markets the rules change. If you beat someone, that person won’t trade the same next time.”

- Ernest Chan, Managing member,

QTS Capital Management

“Everybody thought that the financial system was like playing chess or a game of Go because AI has been outperforming humans in all these games,” said Ernest Chan, an expert in quantitative trading who is the managing member of QTS Capital Management, a Canadian investment fund that specializes in intraday futures and FX trading. “Unfortunately, the financial markets are not the same as these games, far from it. In the financial markets the rules change. If you beat someone, that person won’t trade the same next time.”

Getting a handle on what banks are doing in the area of machine learning is challenging because relatively few are willing to reveal the details of their initiatives, particularly in sensitive areas such as trading. But over the past year a number of examples have come to light through presentations at conferences, interviews in technical journals, and publicly announced partnerships with startups specializing in artificial intelligence.

In this article, MarketVoice takes a look at five examples of these initiatives:

- At J.P. Morgan, one of the leaders in the field, one application involves using machine learning in equities market making.

- At ING, the fixed income division is harnessing predictive analytics to help pricing decisions for bond traders.

- UBS is using a specialized form of machine learning to create better strategies for trading options.

- At Standard Chartered, two quantitative analysts in the financial markets division are exploring the use of machine learning to reduce the cost of initial margin for swaps.

- BNP Paribas is using a combination of machine learning and natural language processing to improve interactions between its securities processing division and its clients.

Market making

One of the banks that has publicly touted its prowess in machine learning is J.P. Morgan, which launched a trading program it dubbed LOXM in 2017. According to the bank, LOXM is a self-teaching trading algorithm which is able to learn from past trades (both real and simulated) in order to execute large and complex equities trades at the best price without moving markets. The bank reportedly began to deploy the system in Europe in early 2017 and rolled it out worldwide at year-end.

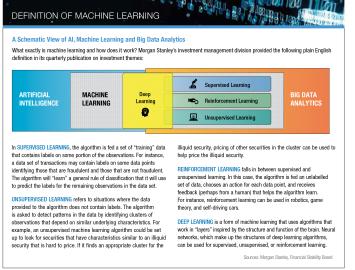

While J.P. Morgan did not respond to a request for an interview, Vaslav Glukhov, the bank’s head of EMEA e-trading quantitative research, discussed LOXM at a conference in May. Glukhov explained that J.P. Morgan used a branch of machine learning called reinforcement learning to train LOXM for limit order placements. Reinforcement learning lies between supervised learning— where some data is given labels—and unsupervised learning, where data has no labels and the computer is asked to find patterns in the data. In reinforcement learning, there are no labels, but the computer receives human feedback that helps the algorithm learn.

“How LOXM is rewarded for being efficient in the market, and how the efficiency of the agency is defined, is stated in the reward function,” Glukhov said at the conference. “We send simulated orders to the exchange, we simulate how they execute, we simulate market impact, and then we feed the reward and batches of execution back to the agent’s brain, which memorizes which actions are good and which are not so good.”

Glukhov explained that the software had to learn how much to place, at what price and for how long. “It needs to be smart in terms of how long it needs to place that order,” he said. “If it gives the order for too long, it will lose the opportunity and it will need to execute at a higher price.”

Predictive analytics

J.P. Morgan is also working with startups that have specialized skills in artificial intelligence. For example, the bank has been working with Mosaic Smart Data, a London-based startup, since October 2017 on ways to use its data analytics engine in its fixed income sales and trading business. In March, the bank stepped up its engagement, making a strategic investment in the company and signing a multi-year contract to use its data analytics across its entire fixed income trading business.

Mosaic Smart Data has built a technology that captures and integrates all of the data flowing through a bank related to client trades, and then uses several types of machine learning to make sense of that data. Using its software, traders can see an integrated set of analytics that captures all dimensions of client flow across the bank. More importantly, the software’s predictive analytics capabilities can help the traders can anticipate what actions their clients might need, such as rebalancing their positions, and even predict when a client may be preparing to depart for another firm, according to Matthew Hodgson, the company’s founder and CEO.

Hodgson came from a trading background at Deutsche Bank and Citi. He decided to start the company because he realized that there was no tool available for getting an integrated view of what his clients were doing.

“I had this enormous frustration that we weren’t able to answer some very fundamental questions about the business and how we could improve the service that we deliver to the clients, and who are most profitable clients were, and what we could do to attract more business from those clients,” Hodgson said in an interview. “We didn’t have the data, the single view of all the business we were transacting, which would give us those answers. I came to the realization that there was a need for a financial market space data analytics company, which could deliver those insights for that particular community, which is really frontline production people in sales and in trading across the various desks within an investment bank.”

Just getting a handle on existing data was a big step forward, but the real value comes from the ability of machine learning to analyze that data and make predictions, Hodgson explained.

“In a fixed income market today most traders only have a historical view. Essentially they’re driving looking in the rearview mirror. The first step is to bring data processing into a real-time view. Artificial intelligence allows us to go a step further and begin making our analysis much more predictive. Sales and trading teams can then see the road ahead much more clearly.”

Another example of a bank using machine learning to support its traders is ING. In December, the Dutch bank announced that it had begun using a streaming analytics platform to help its fixed income traders collect better bond prices. The trading system, dubbed Katana, uses machine learning to plow through hundreds of thousands of trades and then generate pricing recommendations for the bank’s bond traders. In a six-month trial on the bank’s emerging market desk, Katana reduced trading times in 90% of trades while achieving a 25% reduction in trading costs.

Trading strategy

UBS is another example of a bank that is exploring the use of machine learning to enhance its trading. The Swiss bank revealed last year that it is partnering with TradeLegs, a New York-based startup that specializes in a sophisticated form of analytics for options. The goal is to develop new strategies for trading volatility on behalf of the bank’s clients.

TradeLegs claims that when it comes to the options markets, even conventional machine learning will be overwhelmed by the number of potential strategies that need to be checked to find the best trade. TradeLegs instead relies on a combination of search optimization and deep learning, a type of machine learning that uses multiple levels of learning layers, similar to the neural network in a human brain. The company says its derivatives decision engine can optimize every dimension of the strategy, including capital, risk and margin, for every combination of puts, calls and the underlying stock over all potential prices and volatilities.

In an interview with the Financial Times in July 2017, Beatriz Martín Jiménez, chief operating officer of UBS’s investment bank, said the bank is using this decision engine to generate an optimization strategy that is then validated by human traders. She added that it probably would be “several years” before the system would be allowed to execute trades on its own. UBS declined to provide any information on the progress since then.

Optimizing margin costs for OTC derivatives is another area where machine learning could play a role. Alexei Kondratyev and George Giorgidze, two experts on quantitative finance working in the markets division of Standard Chartered, published a research paper on this topic in October 2017.

The two analysts focused on the challenge of reducing the amount of initial margin required on a portfolio of uncleared interest rate swaps and foreign exchange forwards. Standard optimization algorithms have a hard time handling the number of variables that need to be taken into account. In addition, some of the variables are non-linear.

Instead, Kondratyev and Giorgidze proposed using two particular types of machine learning called genetic algorithms and particle swarm optimization. Both types are based on an evolutionary approach to learning, i.e. the system learns incrementally from repeated cycles of results that are affected by mutation, crossover and survival of the fittest.

In this case, the system simulates a set of trades aimed at reducing initial margin, then discards the ones that increase margin costs and keeps the ones that lower margin costs, and then repeats the process over and over again. In addition, the surviving trades are recombined in various ways to create “offspring” that produce better results in the next cycle.

The paper was published as academic research, but it appears that the bank has begun using the techniques. According to a December article in Risk magazine, Standard Chartered has been using these two types of evolutionary algorithms to reduce margin costs since the beginning of 2017.

Broken trades

French bank BNP Paribas is also investing heavily in artificial intelligence. While the bank declined an interview request, its executives described two of its projects in an article published in Securities Finance Monitor, a trade publication.

One project, called Smart Chaser, is being deployed in its securities services division. The tool analyzes thousands of failed trades across 100 individual factors, then matches those factors against existing trades to predict which trades might fail. Initially, Smart Chaser will help the bank’s middle office team focus on the most problematic trades before they become a settlement issue.

The goal is to reduce the amount of manual intervention in the processing of trades for the bank’s clients, explained Thomas Durif, global head of middle office products at BNP Paribas Securities Services.

“Using predictive analysis, Smart Chaser will analyze historical data to identify patterns in trades that have required manual intervention in the past and proactively warn clients and their brokers on their live trading activity so they can take action promptly,” Durif said last fall when the bank announced the initiative. “We are already making good progress, having reached around 98% prediction accuracy.”

BNP Paribas also is applying natural language processing, a different branch of artificial intelligence, to create a “virtual assistant” capability for Neolink, its client reporting platform. The goal is to create “cognitive algos” to help clients mine information and find results quickly, the way voice recognition tools work in the consumer world. NLP enables computers to understand, process, and generate language just as humans do, and it is being harnessed by banks to analyze emails, social media and texts coming from their clients.

Outreach

Like J.P. Morgan and UBS, BNP Paribas has created an innovation lab to explore the potential of machine learning and other advanced technologies. All three banks also have created innovation labs where startups can work side by side with their own staff.

This approach reflects a general trend— banks are reaching out for expertise. Broadridge, a New York-based company that provides trade processing services for securities markets, conducted a survey of 197 financial services executives at a recent conference and found that 96% were inclined to work with a third-party firm to implement artificial intelligence because such partnerships take advantage of shared costs.

Broadridge itself has begun exploring ways to use various forms of AI in its services. For example, the company sees a potential use in collateral management. A firm could use machine learning to analyze historical data and then predict the amount of collateral its counterparties will need. The company also has developed a machine learning tool that reads unstructured data on emails and faxes from clients dealing with block trades and automates the division of block trades to individual accounts.

Mike Alexander, CEO of Broadridge, points to compliance and risk management as areas where AI offers a lot of promise. “Historically, in these areas you’d have to look at a lot of data and you’re trying to find the needle in the haystack,” he said in an interview. “Machine learning can help you find the needle better and give you insights.”

Red flags

While AI can now be used to find illicit activity, there is also growing concern that an AI robot might itself do something that causes systemic disruption, such as provoking a flash crash.

The risk in these types of systems is that the machine learning is trained on a set of historical data, and then a regime change comes along that changes the relationships among the data. Markets are complex networks that are in a constant state of flux, and therefore require a different approach, according to Marcos López de Prado, an expert on quantitative investing and machine learning, who recently joined AQR.

“When developing machine learning investment strategies, most researchers overfit their models to an historical scenario that will not reoccur again,” said López de Prado, whose career includes stints at Tudor Investment Corporation, Hess Energy Trading and Guggenheim Partners. “Researchers coming from other machine learning fields may not know how to prevent overfitting in finance.”

These concerns are so great that the Financial Stability Board, the international body backed by the Group of 20 countries, warned last fall that the definition of the global financial system needs to be expanded to include new high-tech players because of network effects, such as when many banks might use one trading platform. The FSB expressed concern that these firms are not currently regulated by national or international financial regulators.

The FSB also warned that applications of artificial intelligence and machine learning could result in “new and unexpected forms of interconnectedness” between financial markets and institutions. For example, this could arise if various institutions use data sources that previously were unrelated.

Third, the FSB warned that the nature of machine learning makes it difficult for supervisors to understand the decisions that emerge from the machine. “The lack of interpretability or ‘auditability’ of AI and machine learning methods could become a macro-level risk,” the FSB said. “Similarly, a widespread use of opaque models may result in unintended consequences.”

This is a challenge even within the banks. Glukhov, the J.P. Morgan quant working on its LOXM market-making system, said the bank needs to explain what the system is doing. “We want to be able to explain it to our clients as well as to regulators and prove that the algos won’t disrupt the markets,” Glukhov said. “We can’t just tell them we did that because we trained the agent and that’s what the machine tells us.”

Nailing down the explanation process may be why the bank recently hired Manuela Veloso, the head of the machine learning department at Carnegie Mellon University, to head its AI research. “We are working on the ability for these AI systems to explain themselves, while they learn, while they improve, in order to provide explanations with different levels of detail,” Veloso said in a recent interview.

Charles Wallace has reported on business and finance for more than 20 years. His articles have appeared in numerous publications including Fortune, Institutional Investor and Time.